ASIC’s fee and cost disclosure regime has been a journey of twists and turns for the superannuation sector and the road ahead doesn’t look any straighter. Whilst disclosing fees and costs in Product Disclosure Statements (PDSs) and periodic statements sounds simple enough, it is costing super funds millions of dollars to get it right. Let’s take a brief look at why RG97 is ‘tangled with good intentions’.

Why is RG97 needed?

High administration fees erode member balances and has the potential to put a big hole in the retirement savings for many. Consumers require consistent and transparent communication when it comes to fees and costs in order to understand the difference between ‘high’ and ‘low’ fees and consider the impact that fees and costs has on their retirement income.

What does RG97 contain?

RG97 provides guidance for issuers of superannuation products and managed investment products on how fees and costs should be disclosed in PDSs, short PDSs and periodic statements. The purpose of fees and costs disclosure is to ensure that consumers have accurate information to help them make confident and informed ‘value-for-money’ decisions, compare products and understand the fees and costs charged to them.

When does RG97 apply?

PDSs given from 30 September 2022 must meet RG97 requirements, although issuers have been able to apply them since September 2020. Periodic and exit statements with reporting periods commencing on 1 July 2021 must comply with the new requirements, meaning that the new requirements for exit statements will be triggered for exits on or after 1 July 2021.

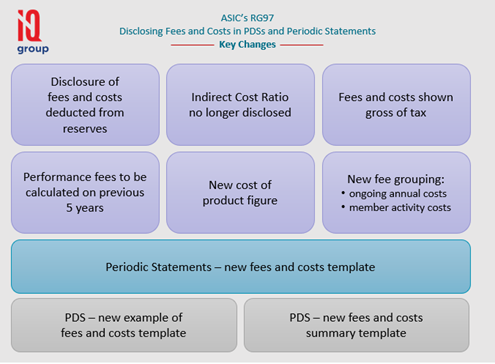

What are the key issues?

- Issue 1 – a prescriptive framework

The legislative framework for fees and costs disclosure is prescriptive and can present many complex compliance challenges for funds. One of the aims for RG97 is for the fees and costs disclosure regime to be practicable to apply for industry while ensuring consumer objectives are met. Applying a prescriptive framework for super and managed investment products that are on very different platforms is difficult, as pricing can be complex and multi-layered.

- Issue 2 – potential to misinform

Some super funds are increasingly lowering their fees and costs in order to stay competitive in the market and some products can be made to look cheaper, and more competitive, than others when in fact they have the same costs. Whilst ASIC has the power to stop disclosure that does not meet legal requirements, consumers can be left misinformed in the process.

- Issue 3 – platform products vs direct investments

Platform operators that provide products such as Master Trusts or lnvestor Directed Portfolio Services (IDPS) could, in theory, reduce overall fees as they are pooled. These fees may apply to administration, moving money in and out, investment management and service. Platform products have a more complex structure and therefore disclosure is also going to be more complex than for non-platform products like “self-directed” investment products.

As the super industry continues to grapple with the fees and costs disclosure regime and ‘untangle’ these key issues, RG97 is ultimately an attempt to further enforce consistent and transparent disclosure of fees and limit the ability for a fund to appear more competitive to consumers than it actually is. While presenting compliance challenges for super funds, any misleading claims about low fees will be treated very seriously by ASIC and the Regulator will continue to intervene against inadequate disclosure.

Overall, disclosure of any means within financial services is tricky and complicated. Regulatory guidelines, such as RG97, will always include hotly contested issues, however it is up to the super industry to work together with the Regulator to navigate the complexities. Accurate disclosure is critical to prevent misinformation and prevent superannuation members remaining confused, disengaged and potentially disadvantaged when it comes to maximising their retirement incomes.

IQ consultants are the leading experts in regards to legislative changes. Across all of our three key services: Advisory; Delivery and Managed Services, we excel in our proactive understanding of how each fund is unique and we build trusting relationships with funds in order to navigate complexities, like those within RG97, and create individual pathways to success.

By Rom Daulo (Consultant)

Recent Comments